New Allegations of Tax Fraud Coming from Houston Housing Authority Surface

This morning I received word from an anonymous source regarding serious allegations of tax fraud coming from the Houston Housing Authority, possibly involving local politicians in Harris County. See below for the details:

Over $5.1 billion of local property tax valuation has been removed from the tax rolls by the Houston Housing Authority (“HHA”) controlled by Houston Mayor Turner. Annually, over $118,000,000 property tax revenue, including $58,000,000 stripped away from independent school districts. Each year, in perpetuity. Without the vote or official approval by a single elected official at HISD, HCC, the Hospital District, the Port of Houston, or all other public entities losing millions of property tax revenue. The Public Finance Corporation (“PFC”) abuse by the HHA has further spread to acquire properties in Ft Bend County, Montgomery County, and Municipal Utility Districts (“MUDs”) - violating bond requirements issued by such MUDs.

Methodology and Policy Issues

This $5.1 billion only accounts for existing apartments converted by the HHA to PFC property tax exempt. The $5.1 billion does not include the economic value of new apartments built or under construction pursuant to the PFC property tax exemption.

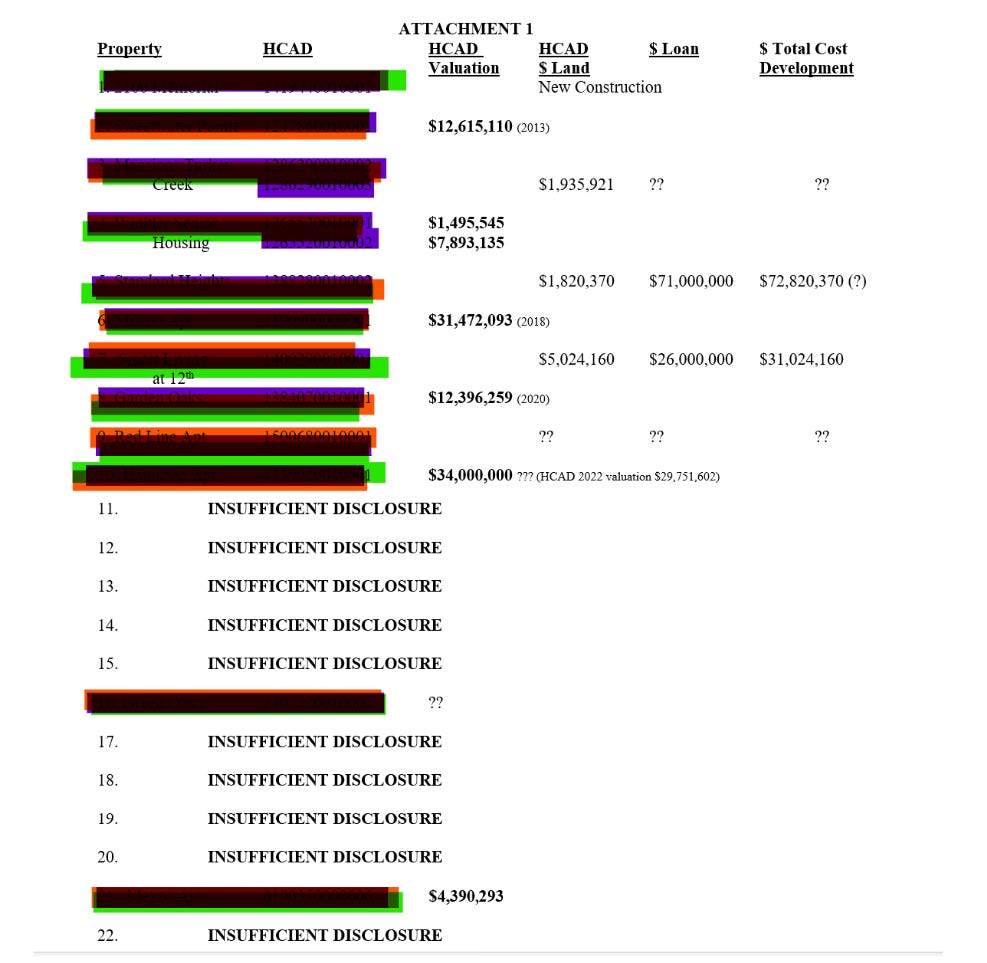

Attachment 1 itemizes known property tax accounts for properties the HHA Board voted to convert to PFC property tax exempt. The Middle Column labeled “HCAD Valuation” identifies the last known property tax valuation before each property became property tax exempt - supplemented with HHA disclosed loan information when the property tax numbers are not available. This methodology understates the actual property tax impact (due to past appreciation and the unlikely assumption each PFC property financing did not include equity – lenders now require up to 40% equity). Attachment 2 sequentially identifies HHA Board Resolutions.

Under the artificial guise of creating “affordable housing”, the HHA recently voted to remove the property taxes from one luxury property HCAD appraised at $102,028,600 ($215,259/unit). Thirty-one (31) of the PFC tax exempt converted properties, including high end midrise complexes, are tax appraised over $50,000,000.

Serious policy issues arise as to whether a 100% property tax exemption is justified by 49% at market rates and 51% at 80% area median income (”AMI”). This criticism is particularly acute when apartments previously rented at 80% AMI are converted into property tax exempt PFC apartments and the reduction in tax revenue does not produce a net gain in affordable units. The HHA deliberately refuses to account for and publish the “net gain in affordability” before and after PFC conversions.

To counter criticism the property tax giveaway does not efficiently create affordable apartments, many private developers proposed PFC conversions with 10-25% of the units at 60% AMI. The HHA Board voted to approve the 60% AMI units. BUT THEN:

Moving Backward on Affordability

Mysteriously (and outrageously) the HHA Board moved backwards on affordability by later voting to convert approved 60% AMI units to 80% AMI (Attachment 3). On at least one property the original HHA Board vote approved 100% of the units at 60% AMI and then later changed the mix to 49% market and 51% at 80% AMI. This grab for extra cash while reducing affordability was apparently orchestrated by insider(s) “coaching” each developer to rename and reincorporate the partnership entity (typically from a Texas entity to a Delaware entity), with no rescoring of the property, with no cross-reference to the prior vote, and no explanation articulated for why the extra revenue was being gifted over to the newly constituted (and secret) partnership.

The deliberate HHA decision to not cross reference earlier HHA Board votes suggests the HHA Board Members were misled as to the import of their vote. It is also suspected that an audit of the new partner members, reincorporated outside of the “eyes of Texas”, will discover conflicts of interests and criminal activity. At a minimum the Texas PFC statute should require public disclosure of each PFC partner and person profiting from Mayor Turner’s property tax giveaway.

Mayor Turner Control over the HHA Board

But why is Mayor Turner singled out, and how does this Mayor allegedly control the HHA? Three years ago, when three Board Members dissented on PFC votes, Turner summarily replaced them (and then HHA President Gunsolley) within the same month. Later, confronted with whistleblowing allegations by Houston Housing Director McCasland, Mayor Turner fired McCasland the next day. Documents establish Mayor Turner directed former HHA Chair Lance Gilliam and real estate partner Licia Green-Ellis to intervene and “manage” the HHA.

HHA Staff self-scored each PFC Property. Many HHA Board approved Properties scored below 2/10 for schools, 0/5 for flooding risk, and 2/10 for reasonableness of developer fees. Questionable HHA Board standards tabled few proposals and blindly approved Resolutions by

7-0 votes. Accordingly, the HHA Board guarantees that children in low-income families will be dumped in underperforming schools as property tax proceeds are diverted away from the ISDs.

HHA Refusal to Produce Public Records

Where does the disappearing tax revenue go? The HHA won’t say because it refuses to publicly disclose its agreements with private apartment owners/developers/managers. And refuses to disclose documents requested under open records requests. It has been gleaned that the HHA receives a relatively modest one-time payment at the conversion of each PFC Property to tax exempt, and then claims a modest back-end share of “net rental income”. Yet expenses and management are controlled solely by each private PFC partner and the HHA receives the leftover table scraps. In this deliberate, opaque scheme, it is believed the vast majority of the property tax exemption” savings” inures to undisclosed PFC partners and persons. Despicably (in a practice pioneered by early PFC profiteer Tom Bacon), PFC management entities are being converted from Texas to Delaware. To further disguise who is pocketing the tax “savings”.

Why are there gaps and blanks in the Attachments 1-3? Because the HHA notoriously refuses to publish public information material to its Board Decisions. The length of lease terms is rarely disclosed but appear to average 75 years (known partnerships where Gilliam participates have 99-year leases). Even after a 2019 Temporary Restraining Order was issued to require PFC Properties be identified - the HHA systematically refuses open records requests.

Noncompliance with Lease Obligations

In Harris County the Appraisal District signed agreements with each PFC owner requiring annual June 30 reports of leasing compliance for the prior tax year. In June 2022 systemic noncompliance with this 2021 reporting was discovered and, after a nudge by private citizens, the Appraisal District issued a letter requiring thirty-day response. On information and belief less than 20 of the PFC Properties responded and the Appraisal District has been called out to revoke 2021 property tax exemption for noncomplying PFC Properties – with penalties and interest.